SAVING FOR A DOWN PAYMENT? Here's what to do.

SAVING FOR A DOWN PAYMENT?

Homeownership is a very important part of personal finance. When you purchase a home, you are buying an asset that helps to build equity. If you decide to rent a place, you are limiting your growth and helping someone else to build more wealth. The first step to owning a home is saving up for a down payment.

In Toronto, the average down payment for a home is $62,000 according to Sotheby's International Realty. That is a lot of money.

As the prices of homes continue to rise in many large cities, it has taken increasingly longer for people to save up money for a down payment. Many people believe that if they are saving a large amount of money for a few years that they should do something with it until they have reached the amount that they need. The goal is that they will help to grow their money while they save.

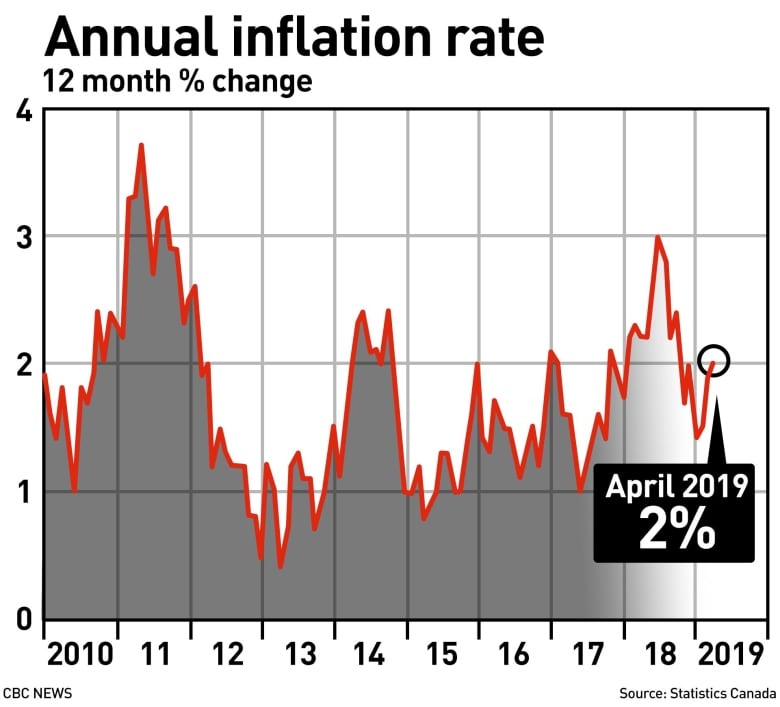

This is a very good idea. If you have money sitting around for years you will LOSE about 2.3% of the value of that money each year due to inflation. Currently, inflation is relatively low, but there have been years when inflation exceeded 5%.

This chart from CBC news displays the annual inflation in Canada since 2010. The rates are very similar to those in the US.

WHAT NOT TO DO?

Many people tend to be very risky when they invest money for a down payment. They do this by investing in the STOCK MARKET.

For the past few years, the stock market has experienced a very strong, and 'bullish' market. This is one of the main reasons why people tend to invest their down payment savings into this market.

The reality is that the stock market is a very volatile market for SHORT TERM investors. If you are planning on buying a home in the next few years, it is important to understand that there is a very high possibility the stock market will eventually crash. This can result in a loss of 40% value of the stocks you own.

Many financial analysists predict that the stock market will crash as early as 2021-2022. This means that if you have that down payment money lying around you should definitely NOT invest it in the stock market for the next few years.

WHAT YOU SHOULD DO?

When you are saving money for a down payment what you should do is place the money in a HIGH-INTEREST SAVINGS account.

The simple reason why you should do this is that you will get very good returns when compared to the low-risk factor. Placing money in a high-interest savings account is almost 100% secure. The only way you could possibly lose the money is if the bank goes bankrupt, which is very uncommon.

Most high-interest savings account have a return of over 2% interest per year. This is much better than the average return of 0.06% of the average savings account. These accounts will help you to maintain the value of your money and even make a small return by the end of the year.

In the following website, it will show the highest paying interest accounts in Canada.

https://www.ratehub.ca/blog/the-best-high-interest-savings-accounts-in-canada/

The first on the list provides a return of 3.30%!

Thank you for reading this post. Please follow me on twitter @money_sleeping. Have a great day and check out some of my other posts!

Homeownership is a very important part of personal finance. When you purchase a home, you are buying an asset that helps to build equity. If you decide to rent a place, you are limiting your growth and helping someone else to build more wealth. The first step to owning a home is saving up for a down payment.

In Toronto, the average down payment for a home is $62,000 according to Sotheby's International Realty. That is a lot of money.

THE PROBLEM

As the prices of homes continue to rise in many large cities, it has taken increasingly longer for people to save up money for a down payment. Many people believe that if they are saving a large amount of money for a few years that they should do something with it until they have reached the amount that they need. The goal is that they will help to grow their money while they save.

This is a very good idea. If you have money sitting around for years you will LOSE about 2.3% of the value of that money each year due to inflation. Currently, inflation is relatively low, but there have been years when inflation exceeded 5%.

This chart from CBC news displays the annual inflation in Canada since 2010. The rates are very similar to those in the US.

WHAT NOT TO DO?

Many people tend to be very risky when they invest money for a down payment. They do this by investing in the STOCK MARKET.

For the past few years, the stock market has experienced a very strong, and 'bullish' market. This is one of the main reasons why people tend to invest their down payment savings into this market.

The reality is that the stock market is a very volatile market for SHORT TERM investors. If you are planning on buying a home in the next few years, it is important to understand that there is a very high possibility the stock market will eventually crash. This can result in a loss of 40% value of the stocks you own.

Many financial analysists predict that the stock market will crash as early as 2021-2022. This means that if you have that down payment money lying around you should definitely NOT invest it in the stock market for the next few years.

WHAT YOU SHOULD DO?

When you are saving money for a down payment what you should do is place the money in a HIGH-INTEREST SAVINGS account.

The simple reason why you should do this is that you will get very good returns when compared to the low-risk factor. Placing money in a high-interest savings account is almost 100% secure. The only way you could possibly lose the money is if the bank goes bankrupt, which is very uncommon.

Most high-interest savings account have a return of over 2% interest per year. This is much better than the average return of 0.06% of the average savings account. These accounts will help you to maintain the value of your money and even make a small return by the end of the year.

In the following website, it will show the highest paying interest accounts in Canada.

https://www.ratehub.ca/blog/the-best-high-interest-savings-accounts-in-canada/

The first on the list provides a return of 3.30%!

Thank you for reading this post. Please follow me on twitter @money_sleeping. Have a great day and check out some of my other posts!

Comments

Post a Comment